Donation of Preferred Shares from Private (CCPC)

Content

Donations of Preferred Shares from Private Corporations is becoming more popular despite significant constraints in the Income Tax Act on the tax advantages to making such gifts. Unlike publicly listed securities, gifts of private company shares do not enjoy the same favourable tax rules regarding the tax on capital gains. In addition, there are complex rules surrounding the donation of private company shares to private foundations that can significantly impair the ability for shareholders to make such gifts to their own foundations. The good news is that these restrictions do not apply to public charities. Therefore Public Foundations like Benefaction can assist in this regard.

For the purposes of this article, the property to be gifted is fixed value, redeemable, preferred shares with or without dividends (e.g. estate freeze shares).

When such a share is redeemed back to the company, unless a capital dividend is used to redeem shares, the shareholder will incur a taxable deemed dividend equal to the excess of the value of the share above its paid-up capital, and dividends are taxed at higher rates than capital gains.

This means more reportable income for the shareholder. However, for the philanthropically inclined shareholder, by donating the same share in specie to the public charity before the company's redemption, the shareholder receives a tax receipt for the value of the proceeds received for the shares, and the transaction does not result in a deemed dividend to the shareholder, which results in more net tax savings from the gift. When the company redeems the shares, the charity shareholder can be paid a taxable deemed dividend, and being tax-exempt pays no tax. The fact that the company paid a taxable dividend to the charity may also result in additional benefits to the shareholder/corporation.

Benefaction Foundation protocols for accepting CCPC Preference Shares:

The Benefaction Donor Agreement completed and signed.

A Deed of Gift for Private CCPC completed and signed.

A signed letter of undertaking from the donors to make the gift.

Written resolution from the CCPC board confirming intent of donation of gift and redemption.

Share Certificates for the preferred shares to be donated.

An acceptable current valuation of the shares. A Chartered Business Valuator (CBV) is the professional of choice for determining this amount.

A cash transfer or cheque for the redemption value. Generally, these shares are immediately converted to cash and the charity issues a tax receipt for the proceeds received for the shares. However, Benefaction will accept a redemption schedule up to a maximum of 15 years provided it is clearly defined in the Deed of Gift.

Legal review of all documentation will be sought by Benefaction prior to gift acceptance.

Why a public foundation like Benefaction and not a Private Foundation?

Notwithstanding the taxation benefits described above, a Donor Advised Fund (DAF) at an arm’s length Public Foundation offers a better solution for CCPC owner with or considering their own private foundation. Just like in his or her own foundation, donors with a DAF can still make recommendations as to how to spend the funds, but unlike private foundations, they are able to maintain more privacy because all directors, donations and grants made from the private foundation are listed on CRA’s website annually for all to see. In a DAF scenario, all donations and grants are still presented but are combined thus making it impossible to know the activities of individual donors.

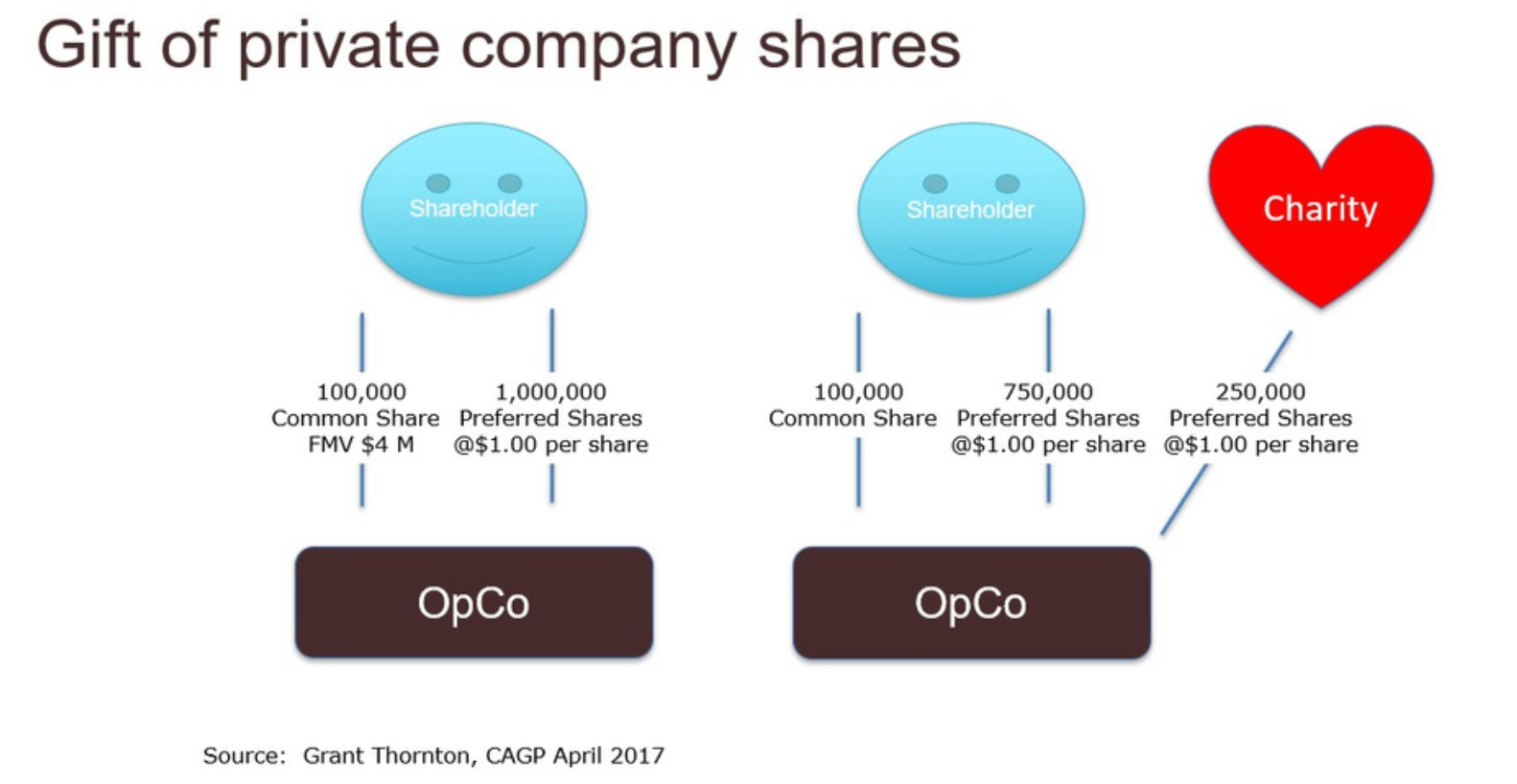

Scenario: The donor is an entrepreneur. The CCPC has thecash to issue a taxable dividend. The donor/shareholder donates private company shares to charity.

Immediately:

Shareholder transfers $250,000 in preferred share to a public charity

Company declares a $250,000 taxable deemed dividend to charity (donor avoids tax on dividends).

Charity returns shares to donor's company and issues a $250,000 receipt to the donor.

Additional tax benefits may be available using this gift plan. Please consult your tax and legal advisors for other shareholder/corporate benefits. Benefaction makes no guarantees, representations or warrantees with respect to this gift strategy.